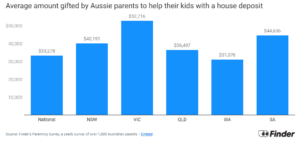

With the cost of living on the rise, it’s natural to want to give your children a helping hand financially. This is especially true as home ownership becomes increasingly out of reach for many young Australians. In fact, according to 2023 data from Finder’s CST, parents give their children an average of $33,278 to help with a house deposit. More than 60% of first-home buyers in Australia now receive some form of financial assistance from their parents to enter the housing market. Collectively, the “Bank of Mum and Dad” is estimated to be worth about $35 billion.

Christine Swanson, Owner and Financial Adviser at Prominent Financial Services, advises, “It’s natural to want to support your children, but your financial security matters too. Finding the right balance between helping your children and protecting your retirement savings is essential. A well-thought-out financial strategy ensures you can assist them without compromising your future.”

Points to Consider Before Gifting Money

It’s certainly possible to provide financial support to your children without sacrificing your own retirement. However, you should consider the following points to protect your financial wellbeing:

1. Impact on Retirement Savings

If you are already retired, withdrawing a lump sum to help your children could reduce your pension payments or erode your savings altogether. With life expectancy rising, there’s a real risk of outliving your savings. If you are nearing retirement, any deviation from your savings strategy could have significant consequences, as there’s limited time to rebuild your superannuation balance.

2. Gifting vs. Loaning Money

While gifting cash carries no tax implications, gifting assets (such as shares or property) can trigger capital gains tax. Moreover, gifting money while receiving government benefits may affect income and asset tests, leaving you financially worse off. A loan, on the other hand, can reduce dependency and establish clear expectations.

Over 50% of kids who borrow from their parents are under financial stress, compared with only 28% of buyers who use their own resources. Lending money with a written agreement can also help avoid favouritism if you have multiple children. Additionally, 7% of parents assist their children by paying the mortgage, and 7% serve as guarantors on loans—figures that have increased since 2019.

3. Document the Agreement

Even when lending to family, it’s important to formalise the arrangement in writing. A properly documented loan agreement outlines the terms of repayment, ensures both parties are clear on expectations and can prevent misunderstandings that could lead to financial loss or damaged relationships. Without this safeguard, it becomes difficult to enforce repayment or even confirm whether the money was intended as a loan or a gift.

A cautionary tale: Dave and Lucy withdrew $131,000 from their superannuation to help their son and daughter-in-law buy a home, expecting the funds would be repaid over time. However, when the couple divorced, the house was sold, and after paying off the mortgage, the remaining proceeds were divided between the former spouses. Since Dave and Lucy had no loan agreement in place, their son and daughter-in-law claimed the $131,000 was a gift rather than a loan. With no legal documentation to prove otherwise, Dave and Lucy were unable to recover the money, creating financial strain and causing lasting tension in their relationship with their son.

This scenario highlights the importance of treating financial arrangements with family as seriously as those with any other borrower. Having a solicitor draft a simple loan agreement can save everyone involved from unnecessary stress and conflict, helping to preserve both your finances and your family relationships.

A Final Thought

Helping your children is a generous act, but you’ve worked hard for your retirement, and your financial well-being should remain a priority. At Prominent Financial Services, we understand the importance of balancing family support with your long-term financial security. “By discussing your financial goals with a professional adviser, you can develop a plan that supports your children, if needed, without compromising your future,” says Christine.

Let us help you set realistic retirement goals that align with your financial needs and family values. With the right strategy, you’ll stay on top of your retirement finances and enjoy peace of mind, knowing you’ve planned for the future. Contact Prominent Financial Services today to ensure your retirement plan is on track—and live your best life, whatever that means for you.

For help and advice, contact our team here.

Sources:

- a) Not for publication (for research purposes)

www.finder.com https://www.finder.com.au/home-loans/bank-of-mum-and-dad

www.servicesaustralia.gov.au Gifting (10 December 2021)

{kind=link}